How to Fund your startup

Overview of this article:

The validation gut check: Are you actually ready to raise, or do you have a validation problem?

Sales first: Why revenue is the most underrated funding source, and how to use AI to build a testable MVP in 2026 for basically £0

Grants decoded: What Innovate UK actually offers in 2026 (and why Smart Grants are paused), plus how to access 1,200+ UK and EU grants

Equity explained: Friends and family, angels, and VCs, who they are, when to approach them, and how to find them

SEIS and EIS: The UK tax relief schemes that make your startup 50% more attractive to investors

Dilution maths: A worked example showing how your 50% becomes 29.5% across three rounds

The full funding stack: What proof you need to move from validation through to Series A+

Read time: 15 minutes.

Best for: UK founders at pre-seed or stage, building in impact, SaaS, consumer, or deep tech.

————————————————————

So… how the hell do you fund your idea?

It's one of the first questions every first-time founder has, and one of the hardest to act on. I know, because I've been there.

Back in 2020, when I started building my first company, The Bug Factory, I thought I'd have clarity by the time I needed money. Instead I sat on it for months. Paralysed by the fear of picking the wrong path. Overthinking every route. Worrying about the cost of getting it wrong.

That's the thing nobody tells you. At the early stage, the biggest blocker isn't money. It's decision fatigue.

It's now 2026, and I talk to first-time UK founders every week who feel exactly the same. They can't start because they haven't figured it all out. And here's the truth: you won't. Not up front. You'll pick a path, learn, pivot, and pick another.

The smartest founders I know don't pick a purist "grants route" or "angel route." They blend:

Sales,

Grants,

Equity

This guide walks you through the funding landscape honestly, without the fluff. So you can stop second-guessing and start moving.

Let's get into it ✌️

0. First things first: are you actually solving a real problem?

Before we talk about a single pound, let's do a gut check.

If you read Part 1: How to Tell If Your Idea Is Worth Anything, you already know where I stand on this. But it's worth saying again, because it's the single biggest reason first-time founders struggle to raise:

Investors don't back products. Grants bodies don't fund clever ideas. Customers don't buy features.

They all back the same thing. A real, painful, frequent problem being solved by the right team at the right moment.

Before you open a pitch deck or Google "SEIS application," answer these three honestly, in front of someone who won't humour you:

What painful, frequent, urgent problem am I solving?

Have I spoken to at least 20 real humans who have this problem?

Have any of them shown me they'd pay for a solution? (Pre-orders, waitlists, LOIs, actual money)

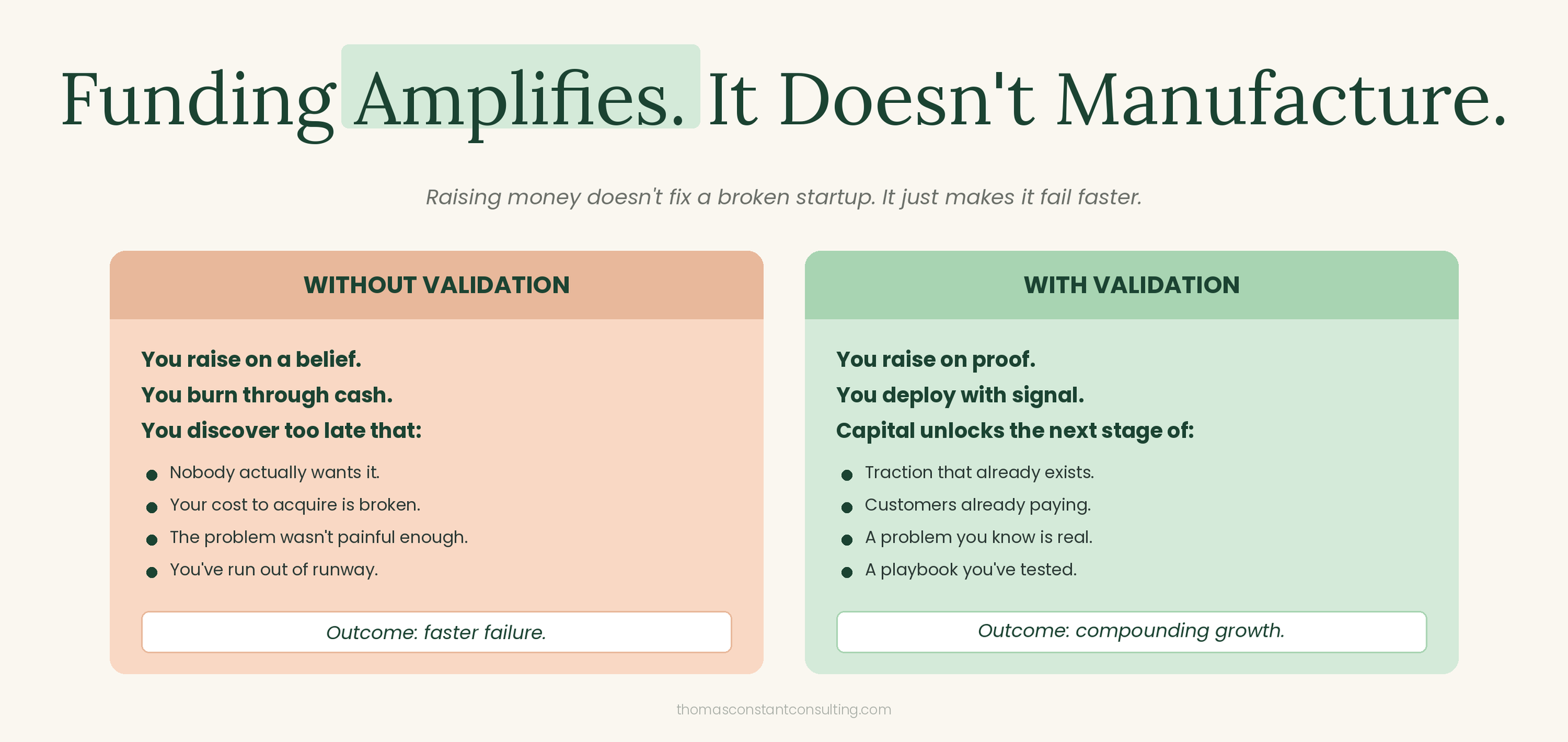

If any of those are wobbly, you don't have a funding problem. You have a validation problem. Go back to Part 1. That's not failure. That's you saving yourself six months and a lot of pain.

Funding amplifies what's already working. It doesn't manufacture it.

1. Sales: The Most Underrated Funding Route

Let's start with the obvious one, that almost no one actually starts with: revenue!

If you can sell your product or service early, even in its roughest form, and make money, do it. That is your best form of funding. It's non-dilutive, immediate, and gives you real customer feedback. Founders get obsessed with raising money and forget that making money is still a thing.

Real sales aren't just money in the bank. They're proof. Investors and grant assessors don't have to imagine demand. They can see it.

Daniel Priestley calls this being 'oversubscribed'. The idea is simple: before you even officially launch, you've already created demand and even secured funding from future customers. Instead of asking for permission or capital, you build so much interest upfront that you effectively self-fund from day one. (His book Oversubscribed is worth every page.)

💸 Sales don't just fund you. They validate you.

If you can get people to part with money early on, that's better than any investor "yes." If you're building something physical or tangible, platforms like Kickstarter and Crowdfunder UK let you pre-sell your idea to the world. If you hit your funding target, you unlock the capital to build it. If you don't, nobody's charged. It's a beautiful signal of market fit and early demand. Use your own site. Use waitlists. Use email sign-ups. Use crowdfunding platforms. But start with sales. That's your strongest early funding tool.

Your early revenue shows traction. It proves people want what you're offering. And when you do go to investors or grant bodies, you're not just talking about a "great idea." You've got proof. Of course, this won't apply to every founder. If you're in biotech, deep tech, or anything with heavy R&D and regulation, you'll need upfront capital. But if you can generate your own oxygen? Do that first.

Use AI to build and test before you spend a penny

Here's what's changed massively between 2020 and 2026, and most founders haven't caught up. If you're a non-technical founder, what used to take £20,000 and three months of a developer's time now takes an afternoon and £0. The AI tool stack in 2026 can get you from idea to testable MVP in a few hours. Here's the current playbook:

Lovable, Bolt.new, v0 by Vercel — prompt-to-app builders. Describe what you want, watch it build. Perfect for web-based MVPs.

Claude or ChatGPT — build landing page copy, outreach emails, customer interview scripts, pricing pages, even simple web apps through Claude's Artifacts feature.

Framer, Softr, Carrd — no-code landing pages that look legitimately professional.

Figma (with AI plugins) or Canva Magic Studio — mockups and visual prototypes, fast.

The goal isn't to build the real product. It's to build something just real enough to test whether people care.

Remember the Airbnb story from Part 1? Their early "platform" had no algorithm. The founders manually arranged stays by phone to prove demand before building real tech. The 2026 AI version is the same playbook: build a fake front-end, handle the back-end manually, learn fast.

Where this gets really powerful is when you combine sales and AI-MVPs.

If you can walk into an investor meeting and show:

"Here's the real problem we discovered through 30 customer interviews."

"Here's the AI-built MVP we tested it with."

"Here's £3,000 in pre-orders we've already collected in 6 weeks."

You're not pitching a great idea. You're pitching a working signal. That's what makes investors lean in.

One more thing. AI-built MVPs are disposable. You're not building a scalable product. You're buying yourself cheap, fast answers to expensive questions. Don't fall in love with the MVP. Fall in love with what it teaches you.

2. Grants: Free Money… or is it?

Grants sound great. And when they work, they are. Non-dilutive. No repayments. No interest. Just capital to help you move forward.

But let's be clear: grants aren't magic. And they're definitely not easy.A grant is money awarded to help you build something specific, usually linked to innovation, sustainability, or social impact. It's given for a reason, not just because your startup has a nice logo.

⚠️ Important 2026 update on Innovate UK

Innovate UK paused its flagship Smart Grants programme in January 2025, with no further rounds in the 2025/26 financial year. So the old "Smart Grants are always open" advice you'll see in older articles is out of date.

What Innovate UK is still running in 2026:

Targeted thematic competitions (net zero, health tech, advanced manufacturing, AI, supply chain, etc.) on the Innovation Funding Service

Innovation Loans for close-to-market SMEs

Knowledge Transfer Partnerships (KTPs) pairing you with a university

Venture Builder Programme pilots for deep tech spin-outs

In other words: Innovate UK is still a massive funder, you just need to watch for the right thematic round rather than waiting for a generic one. There are also plenty of other grant pots out there:

Local growth hubs and LEPs

Bank-led initiatives (NatWest Accelerator, Barclays Eagle Labs)

University innovation centres

Charitable foundations and trusts

Sector-specific funds (climate, food, health, SDGs)

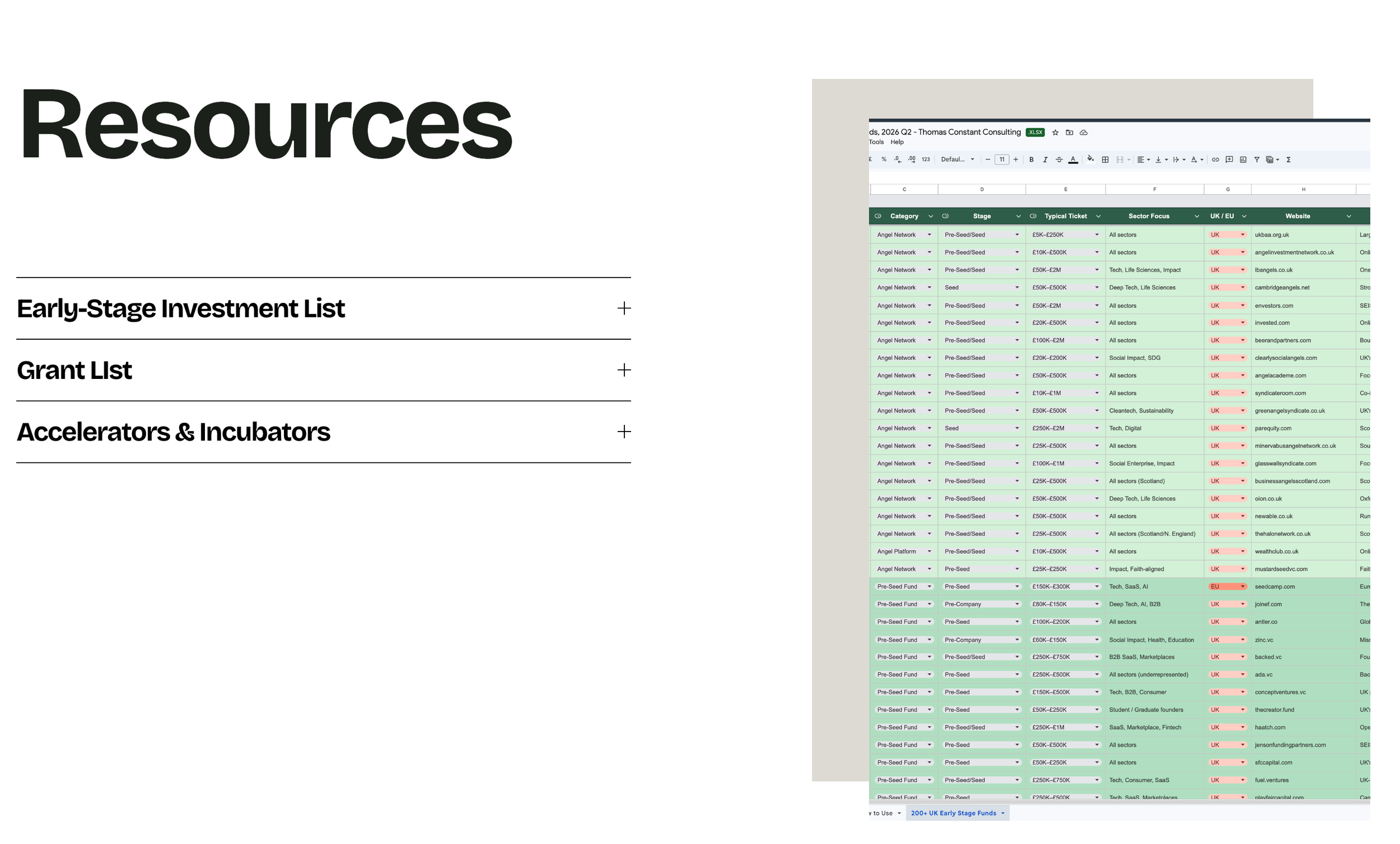

👉 I've pulled together 1,200+ UK and EU grants, plus 210+ investors, accelerators and sector funds into my free Funding Finder. Access it here: thomasconstantconsulting.com/funding-finder

The strings to be aware of

🔥 Grants are highly competitive: Everyone wants free money. Grant pots are limited. Innovate UK Smart Grants historically saw around 4 to 5% success rates for unsupported applicants. The bigger the grant, the tougher the odds.

⏳ They're time-consuming: A proper application takes weeks. You'll need a clear problem-solution statement, defined outcomes and metrics, risk assessments, a credible budget with justification, partner organisations (for collaborative grants), and sometimes detailed financial forecasts. This is not a side task.

💸 They often require match funding: Most large grants won't cover 100% of your project. You might need to cover 30 to 50% from revenue, investment, or other funding. No match funding, no eligibility.

📅 Most grants are reimbursed, not paid upfront: Let's say you win £500K. You don't get a cheque on Day 1. You spend the money first, then reclaim it (usually quarterly). You'll need short-term cash flow to fund the project while you wait for reimbursement.

📋 You'll get a monitoring officer: Someone whose job is to keep an eye on how you're spending the money. Expect quarterly check-ins, budget reports, and evidence of outputs. Every pound needs a plan.

Grants are brilliant when done right. But they can also be a trap. Some founders become grant-chasers, warping their company to fit whatever's being funded. Don't do that. Build the company you believe in, not the one that ticks the most boxes on a funding form.

3. Equity Investment: The Art of Selling Ownership

Equity investment means someone gives you money in exchange for ownership of your company. You're not taking a loan. You're giving away a percentage of your business in return for capital, support, and (hopefully) alignment on your mission.

Done right, it's a powerful tool for growth. But you need to be clear about what you're giving up and what you're getting.

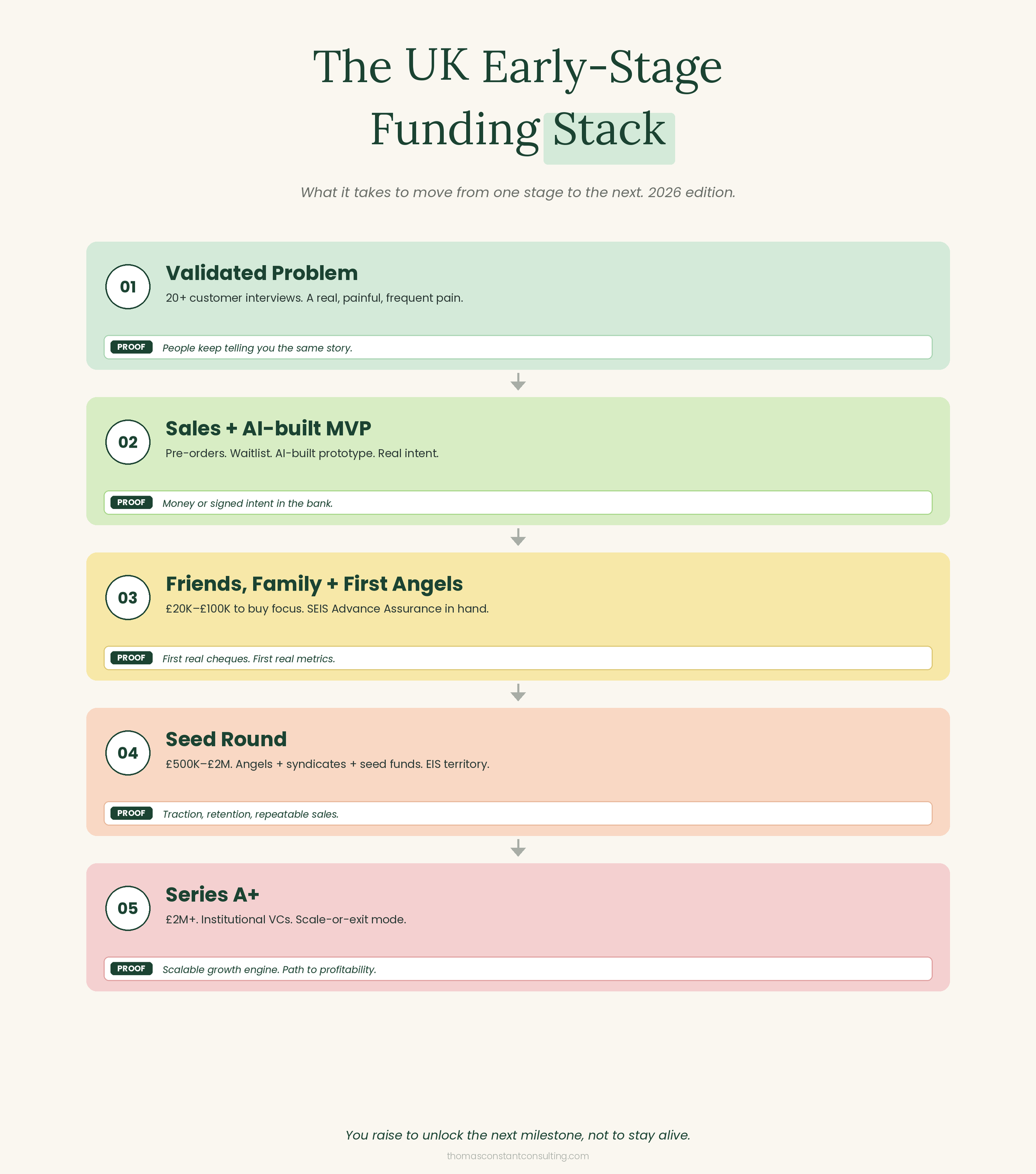

What the Funding Stages Actually Mean. You'll hear terms like pre-seed, seed, and Series A thrown around a lot. There are no fixed rules. These are loose reference points.

1st: Pre-seed

🧪 Stage: Idea to early MVP. Maybe a basic prototype.

💷 Raise size: £100K to £500K

🧠 Investor type: Angels, friends & family, small syndicates, pre-seed funds

📌 What matters: Founding team, vision, early validation (surveys, waiting lists, first pre-orders)

At this stage, you're raising based on belief. Investors are backing you, not your traction. Don't over-optimise. People are investing in you.

2nd: Seed

🌱 Stage: MVP live, early traction, first paying users

💷 Raise size: £500K to £2M+

🧠 Investor type: Angels, seed-stage funds, early VC firms, family offices

📌 What matters: Product-market fit signals, real usage data, team growth, early revenue

Now you're raising to accelerate, not explore. You've proved the concept. You should know your core metrics: CAC, churn, runway, burn rate. You should have a clean cap table and a professional data room.

Onwards: Series A, B, C (and beyond)

🚀 Stage: Growth mode. Real traction. Repeatable sales.

💷 Raise size: £2M to £20M+

🧠 Investor type: Institutional VCs, growth funds, strategic investors

📌 What matters: Serious traction, scalable ops, strong retention, path to profitability

This is where you go from "startup" to "company". Investors look at margins, LTV, MoM growth, retention cohorts, hiring plans, international expansion.

🧠 Rule of thumb: Raise enough for 18 to 24 months. Bring it in upfront. Fundraising typically takes 6 months start to finish. Raise what you need to hit your next milestone, and be able to explain clearly why you're raising, how much, and what it's for.

4. There are three main types of equity investment:

i) Friends, Family, and Fools

👥 Who: The people closest to you, the ones who believe in you, not necessarily your startup

💷 Amount: £1K to £20K total

📌 Stage: Idea, pre-MVP, concept-only

As the name (jokingly) suggests, these are often the first people to give you money when you have nothing but a vision. It's highly risky, and they know it. Or at least, they should.You don't have traction yet. You probably don't have a deck. What you do have is people who trust you personally. So they chip in. They back you, not the metrics.

This capital might fund your MVP, buy you time off your job, or cover initial legal costs. It often makes the difference between an idea that stays on the back burner and one that gets moving. Of course, this route depends hugely on who you know, and that's a real socio-economic issue in startup ecosystems. Not everyone has access to this network, and that's worth naming.

ii) Angel Investors: The Believers

🕊️ Who: High-net-worth individuals who invest personal money into startups

💷 Amount: £5K to £200K per angel

📌 Stage: Pre-seed to seed

Angels are your bridge from "just an idea" to a real, funded startup. They're often founders themselves, or experienced operators who've made money and now want to back the next generation. Some are purely financial. Others are strategic and hands-on.

Unlike VCs, angels invest their own money. They can move fast and decide based on gut feel, founder fit, or mission alignment. But they want more than a return. They want to feel excited, included, and confident in you.

If you're raising your first "proper" round in the UK in 2026, you're almost certainly raising it from angels, either directly or via syndicates (groups of angels pooling capital together).

iii) Institutional Investors: The Big Guns

🏛️ Who: Venture capital firms, early-stage funds, corporate investment arms

💷 Amount: £500K to £20M+ per fund

📌 Stage: Seed, Series A and beyond

Institutional investors are professional investors. They manage other people's money and are expected to return a profit. They're metrics-driven, cautious, and won't invest unless you've already shown traction, revenue growth, and a scalable path forward. They come in after angels, when you've proved that your product has legs.

VCs want big outcomes. They're playing for 10x+ returns, so they'll push you for scale. They also write bigger cheques, which means giving up a larger stake and taking on more expectations.

Most early-stage founders won't deal with VCs straight away. But it's good to understand how they work and how the game changes once they're involved.

5. Finding and Approaching Angel Investors

Here's the thing nobody tells you.

Unlike VCs and institutional funds, angels are really hard to find. VCs have websites. They have theses. They announce when they've closed a new fund. Angels don't. Most of them don't want to be found, because visibility means a flood of cold pitches they'll never read.

There's no clean database. There's no "angels.com". You have to go dig them out.

Here's how.

Tactic 1: LinkedIn

This is the best starting point in 2026 and costs nothing.

Go to LinkedIn, type "angel investor" into the search bar.

Click People in the filter (not companies, not posts).

Filter by 2nd connections so you've got at least one mutual in common.

Filter by lcation (e.g. United Kingdom).

Hit search.

You'll get a list of real UK angels who are one warm intro away. A lot of them literally have "Angel Investor" in their LinkedIn headline, because that's how they signal they're open to deal flow.

Send them a short, personalised message. Not a pitch. A genuine opener that references something specific about them or their portfolio. The goal of message 1 is a reply, not a cheque.

Tactic 2: Search around angels, not just for them

Same LinkedIn approach, but swap the search term. Try:

"angel syndicate"

"angel fund"

"angel group"

"early-stage investor"

"SEIS investor"

Each of those pulls up different networks of people who gather angels together. Syndicates are gold. One yes from a syndicate lead often means 5 to 15 individual cheques from their network, not one.

Tactic 3: Use my Funding Finder

I've spent a stupid amount of time pulling together a list of 210+ UK and EU early-stage investors, syndicates, and accelerators so you don't have to. It sits inside my free Funding Finder alongside the grants list.

Open it up and go to the Early Stage Investment List tab. 👉 thomasconstantconsulting.com/funding-finder

Don't open with a pitch. Open with a question. Be personable. A 15-minute coffee for advice is a much easier "yes" than a 30-minute pitch. If the fit is real, the pitch will happen naturally a few conversations in. If it isn't, you've still built a relationship and learned something. Equity investment is not Dragon's Den. You're not standing in a room with a spotlight. You're chatting to one or two people, often at an event, over coffee, or on Zoom. It's a conversation, not a courtroom.

6. Finding VCs (and when to actually approach them)

Let me be blunt. Most early-stage founders should not and will not be talking to VCs.

I hear it all the time. Founders who've spent months pitching VC after VC, getting ghosted, coming out deflated, wondering what they're doing wrong. The answer is almost always the same: they weren't ready, and they didn't know it. So before we talk about how to find VCs, let's talk about when.

VCs are not angel investors. Do not confuse them.

Angels write personal cheques based on belief in you. VCs write institutional cheques based on metrics, traction, and a defensible path to a 10x return. They are not your friends. They are not the devil either. They are professionals deploying someone else's money, and they are accountable to their own investors (called Limited Partners or LPs) for every pound.

The moment you take VC money, the game changes. You're signing up for:

Accelerated growth expectations: They want their money to grow 10x, 20X… 50X, not 2x

Board seats and reporting: Formal governance, monthly updates, KPIs

Pressure to raise again: Every round sets the bar for the next

Exit: A big sale or IPO, not a lifestyle business

That's fine. That's the trade. But if you're not ready to play that game, VC money becomes a trap, not a gift.

When you actually should be talking to VCs

In my opinion, you should not seriously approach a VC until you have:

Substantial monthly recurring revenue (not just revenue. Recurring. Predictable.)

Clear product-market fit signals (retention, referrals, organic growth)

A proven, scalable acquisition channel (you know exactly what £1 in gets you out)

Raised from angels or received grant funding (you've already done the small-cheque round)

If you're missing any of those, spend your time building traction. Not pitching.

When it's fine to put VCs on your radar

Now, there is nuance here. It's fine to follow them on LinkedIn. Engage with their content. Send the occasional thoughtful update on your progress. Ask for introductions to angels in their network. Just don't pitch them. Build the relationship. Then when you're ready, you're not a cold email. You're a founder they've been watching for 12 months.

How to find VCs (this part is the easy bit)

Unlike angels, VCs are extremely easy to find. They want to be found. Their whole business model depends on deal flow.

They have websites. They publish their thesis. They name their partners and sector focus. Their portfolio companies are all public. There are dozens of free and paid databases. A 10-minute Ai Search gets you most of the UK VC landscape.Some quick ways to find them:

AI Search "UK seed VC [your sector]" and the top 10 results will be most of the active funds

LinkedIn search "Partner" + "Venture Capital" + location filter

Crunchbase, Dealroom, Beauhurst for data on who's actually deploying

Portfolio-matching — find a company similar to yours, look at who invested, approach those funds

Or just use my list

My Funding Finder includes a full list of UK and EU early-stage VCs, sorted by stage, sector, and cheque size. Same spreadsheet as the angel list.

👉 thomasconstantconsulting.com/funding-finder — open the Early Stage Investment List tab.

The bottom line: VCs are easy to find and hard to get. Angels are hard to find and easier to get. If you're pre-revenue or just hitting product-market fit, spend your time on angels, SEIS, and real customer traction. Approach VCs when the numbers speak for you. Not before.

7. Understanding Valuations and Dilution

This is the single most misunderstood part of raising money, and it's the one that hurts the most when you get it wrong. Let's walk through it properly.

The basics: what dilution actually is…

When you raise equity, you're issuing new shares to your investor in exchange for their cash. The total number of shares in the company goes up. Your shares stay the same, but they now represent a smaller slice of a bigger pie. That's dilution. Your percentage ownership goes down with every round. This is not inherently bad. Owning 40% of a £10M company is worth more than owning 100% of a £500K company. The whole point of raising is to grow the pie faster than your slice shrinks.

But founders get this wrong all the time, because they focus on the round in front of them and forget that every future round will dilute them again. By the time you hit Series A, you could own way less than you planned and therefor this makes your uninvestable to future funds as you do not have enough skin in the game anymore.

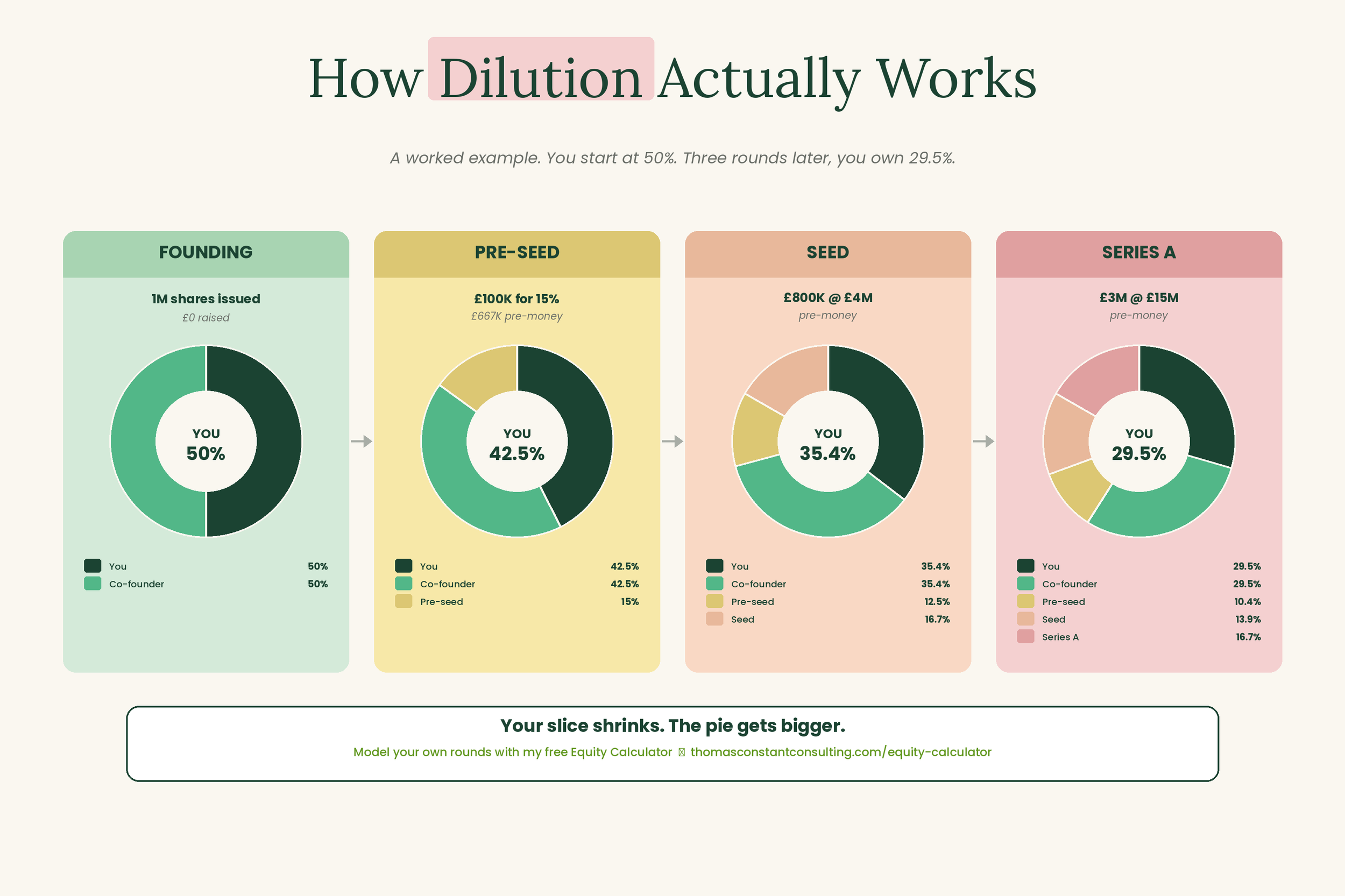

A worked example (because this is easier with numbers)

Let's say you and a co-founder each own 50% of a company with 1,000,000 shares total.

Pre-seed raise: £100K for 15%

You issue new shares to give your investor 15% of the company post-raise.

Your 50% becomes 42.5%

Co-founder's 50% becomes 42.5%

Investor owns 15%

Company valuation: £667K pre-money, £767K post-money

So far so good.

Seed raise 18 months later: £800K at £4M pre-money

The investor gets 16.7% (£800K / £4.8M post-money). Everyone else gets diluted by that same proportion.

You drop from 42.5% to 35.4%

Co-founder drops from 42.5% to 35.4%

Pre-seed investor drops from 15% to 12.5%

New seed investor owns 16.7%

Series A two years later: £3M at £15M pre-money

The Series A lead gets 16.7%. Everyone else gets diluted again.

You drop from 35.4% to 29.5%

Co-founder drops from 35.4% to 29.5%

Pre-seed investor drops from 12.5% to 10.4%

Seed investor drops from 16.7% to 13.9%

You started at 50%. Three rounds in, you're at 29.5%. That's normal. Anyone who tells you otherwise has never raised money.

The rules of thumb that keep founders from getting crushed

Don't give up more than 15 -20% in your 1st proper round. Anything more and you're short-changing every future round.

Model at least 3 rounds ahead before agreeing to any single one. What you give away now compounds.

Protect your voting control. Dilution of economic ownership is one thing. Losing control of decisions is another. Keep an eye on voting rights and board composition.

Valuation isn't everything. A higher valuation with bad terms is worse than a lower valuation with clean ones.

Model it before you sign it

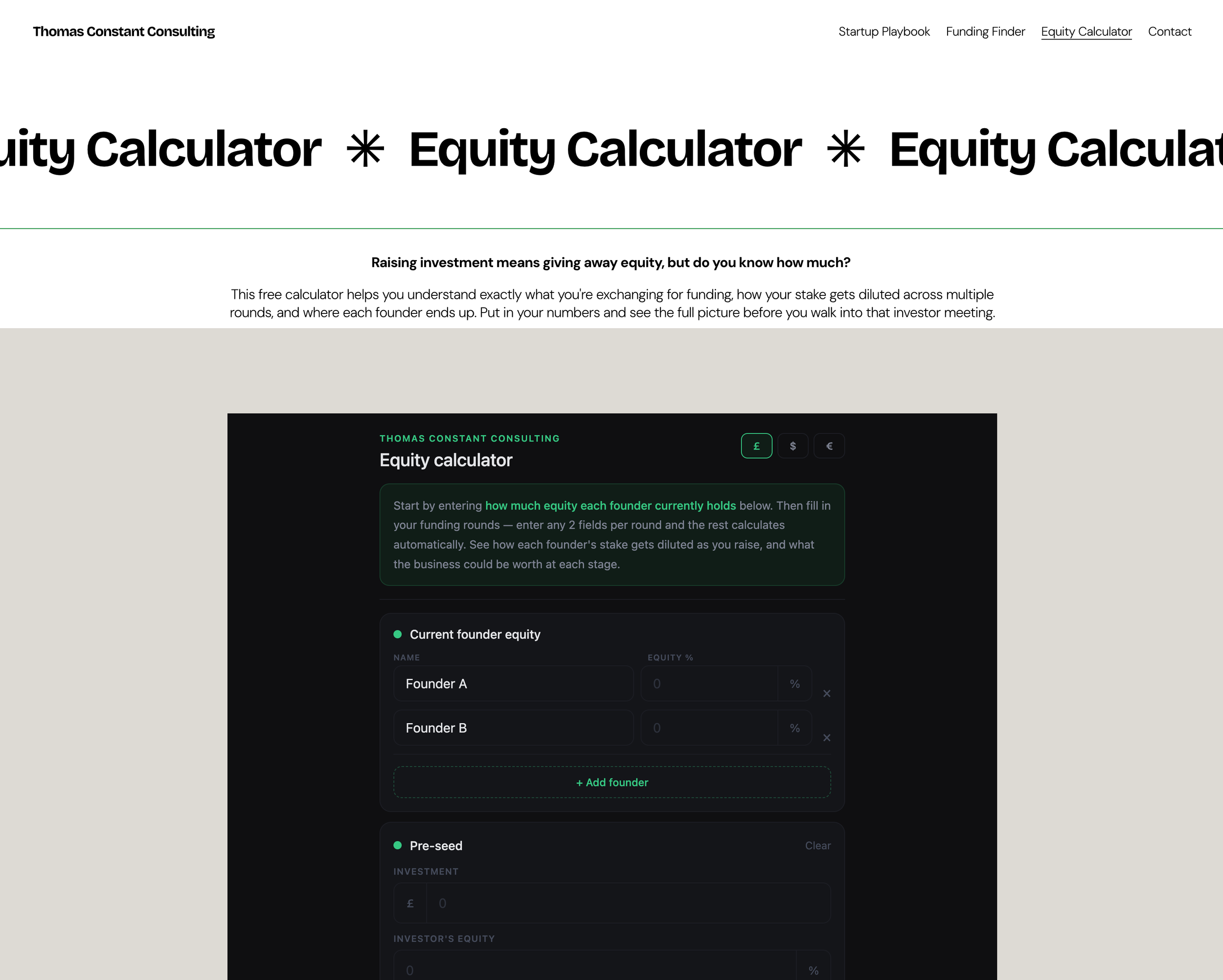

The best way to understand dilution is to play with the numbers yourself. See what happens when you change the raise amount, the valuation, the option pool size. Watch your slice shrink in real time. Once you've done it a few times, you'll stop getting surprised at term sheet stage. I built a free Equity Calculator that does exactly this. Plug in your numbers, model multiple rounds, see where each founder and investor ends up.

The bottom line

Dilution isn't the enemy. Ignorance about dilution is. Every founder I know who feels bitter about their cap table says the same thing: "I didn't realise it would add up like this." Don't be that founder. Understand the maths, model the rounds, and walk into every conversation knowing exactly what you're trading.

8. Know Your Tax Tools: SEIS & EIS

This is where a lot of first-time founders don't realise the UK is genuinely one of the best places in the world to raise at the early stage.

If your company qualifies for SEIS (Seed Enterprise Investment Scheme) or EIS (Enterprise Investment Scheme), investors can claim back up to 50% or 30% of their investment in tax relief, and pay no Capital Gains Tax on profits if they hold the shares for 3+ years.

That's a game-changer. It de-risks the cheque completely. It's one of the main reasons UK angels back risky startups at early stages.

SEIS: Companies can raise up to £250,000 total, investors get 50% income tax relief on up to £200K per year

EIS: Larger rounds, investors get 30% income tax relief on up to £1M per year

To access either scheme, you apply to HMRC for Advance Assurance before raising. It's free. You can do it yourself. And it's one of the biggest unlocks in UK fundraising, full stop.

I'm going to do a full deep-dive article on SEIS and EIS:

Exactly what both schemes are and who qualifies

A step-by-step DIY walkthrough of the Advance Assurance application (no, you don't need to pay an accountant £1K to do this)

The common mistakes that get applications rejected

How to position your raise to investors using the tax relief as a hook

The compliance steps after you raise, so investors actually get their relief certificates

For now, just know this: if you're raising in the UK and you don't have SEIS Advance Assurance in hand before your first angel conversation, you're making your life 10x harder. Angels will ask for it. Some won't invest without it. Start the conversation with "we're SEIS approved" and you've already passed the first filter.

🧠 The TL;DR

Funding a UK startup in 2026 isn't one-size-fits-all. Here's what actually matters:

Validate first. Funding amplifies what's already working. If you don't have real customer proof, you don't have a funding problem, you have a validation problem. Fix that first.

Sales beat everything. Revenue is the most underrated funding source. Non-dilutive, instant, validating. Start here.

Use AI to build lean. In 2026 there's no excuse to spend £20K testing an idea. Lovable, Bolt, v0, Claude, Framer. Ship an MVP in an afternoon.

Grants are free money, but not easy money. 4 to 5% win rate. Weeks of admin. Match-funded. Reimbursed, not upfront. Worth it if the fit is right.

Equity means giving away ownership. Understand dilution before you sign anything. Your 50% won't stay 50%.

Angels are hard to find. VCs are easy to find but hard to get. Know the difference.

Don't pitch VCs too early. They'll tell you no, and they'll remember. Wait until you have MRR and product-market fit.

Get SEIS Advance Assurance. It de-risks the cheque for every UK angel. If you're raising in the UK and you don't have it, you're making your life 10x harder.

Be prepared before you pitch. Know your numbers. Know your traction. Know your story.

Blended wins. The smartest founders blend sales, grants, and equity. They don't pick one lane.

The bottom line: Start with proof. Blend your funding. Protect your cap table. And stop waiting for permission.

———————————

———————————

🧠 Core Reads

Oversubscribed by Daniel Priestley — building demand before you build product. The bible for founders who want to pre-sell.

Angels by Jason Calacanis — a sharp, no-fluff guide to how angel investors think, what they look for, and how to actually get a yes.

Venture Deals by Brad Feld & Jason Mendelson — the standard reference on term sheets, valuation, and investor dynamics. If you're raising equity, read this

The Lean Startup by Eric Ries — the OG framework on MVPs and validated learning. Still relevant.

The SEIS/EIS Guide b — everything you need to know about the UK's biggest early-stage investment advantages. HMRC

Y Combinator Library — Free. Modern. The best collection of founder essays on the internet.

Want Help Applying This to Your Startup?

♻️ Book a free 30-minute Investment Readiness Clarity Call. No pitch required. Just an honest conversation about where you are and what to focus on next.

🔔 Book your free call at thomasconstantconsulting.com