How to Become Investment Ready

Overview of this article:

Why you're really raising: the question every founder skips and pays for later.

Speak Investor: the 30 terms you need to know before your first call.

Stop chasing VCs: why angels are the right first stop and what the investor ladder really looks like.

Build a clean data room: the folder that decides whether anyone takes you seriously.

The raise funnel: turning curiosity into signed cheques, stage by stage.

SEIS, EIS & valuation: the UK-specific edges that change the maths.

Read time: 15 minutes

Best for: UK founders preparing for their first equity raise, pre-seed to early seed.

——————————————————

Getting funded isn't about having a flashy deck. It's about being credible. Professional. Investable.

And in early-stage startups, credibility is everything. You're asking someone to back you, not just your product. You.

That means getting your house in order before you start knocking on doors.

Most full rounds, from first pitch to money in the bank, take six to nine months. Most founders underestimate how much groundwork sits behind that first cold email.

You don't need a Harvard MBA or a Silicon Valley pedigree to do this right. You need to be prepared, professional, and clear on what you're building and why it matters. That's what this article is for.

This is Part 3 of the UK Startup Playbook. If you haven't validated your idea yet, start with Part 1: How to Tell If Your Idea Is Worth Anything. If you're not sure equity is even right for you, read Part 2: How to Get Funded first. They both feed into this one.

1. Get Your Head in the Game

Before you open a single spreadsheet or fire off a cold email, pause. Take a breath. Ask yourself one question:

Why am I raising money in the first place?

Raising capital isn't a rite of passage. It's not a badge of honour. It's a serious strategic decision, and for many early-stage founders it becomes a costly distraction if you're not ready or clear on what it really means.

When you raise equity, you're selling part of your company in exchange for cash. That's it. You are literally giving away a piece of the thing you're building, your vision, your equity, your upside, to someone else.

In return, your investor expects a return. Most angels and all VCs operate on the same basic model. They're looking for companies that can grow fast and either get acquired or go public. In reality, acquisition is the most common outcome.

So before you line up pitch calls, get clear:

Do you actually want to raise equity?

Are you prepared to bring investors into your cap table?

Are you okay being pushed to scale quickly and sell down the line?

Is this a business you want to run, or one you want to build and exit?

If that's not for you, that's totally okay. You might want a company that funds your life, gives you freedom, and pays the bills. Nothing wrong with that. In fact, it's smart.

If that's the case, there are other ways to fund your idea. You can build lean, grow with revenue, apply for grants, or crowdfund your way to early traction. I cover all of those in including the order to try them in.

If you are raising equity, make it count.

Have a plan. You're not raising to "stay alive". You're raising to hit something specific. Product development, key hires, market entry, traction milestones. You raise to unlock growth. Then you prove it. Then you raise again on stronger terms. That's the flywheel.

Raising money is hard. It's slow. It's emotional. It's full of rejection. So if you're going to do it, do it with conviction. Know why. Know what you're giving away. Know what you're trying to achieve.

Because the first person you need to convince is you.

2. Speak Investor Before You Pitch Anyone

Here's the bit nobody warns you about. Walk into your first investor meeting without the vocabulary, and you're done in five minutes.

Investors don't expect you to be a banker. They do expect you to know your own deal. If they say "what's your pre-money?" and you blink, you've lost the room. If they ask "are you SEIS approved?" and you say "I think so, what's that?", same outcome.

This is the language of the room you're walking into. Learn it before you book the meeting.

Money & equity

Equity: a slice of ownership. Shares in your company.

Cap table: the spreadsheet showing who owns what %.

Pre-money valuation: what your company is worth before new money goes in.

Post-money valuation: pre-money plus the new investment. This sets ownership %.

Dilution: your % shrinks each round as you issue new shares. The pie gets bigger.

Runway: how many months until your cash runs out.

Burn rate: how much you're spending each month.

SEIS / EIS: UK tax relief schemes. Your investors can claim back up to 50% of their investment.

People & roles

Angel investor: an individual writing a personal cheque. Usually £5K to £100K.

High net worth (HNW): self-certified wealthy individual allowed to invest in private companies.

Sophisticated investor: self-certified as understanding startup risk.

Lead investor: the first major cheque in a round. They set the terms. Others follow.

Syndicate: a group of angels investing together behind a lead.

VC (Venture Capital): a fund managing other people's money. They want 10x outcomes.

LP (Limited Partner): the pension funds and rich families that fund VCs.

GP (General Partner): the actual humans running a VC fund.

Stages & rounds

Bootstrapped: self-funded. No outside equity yet.

Pre-seed: first money in. Idea plus early MVP. £50K to £500K typical.

Seed: real product, early traction. £500K to £2M typical.

Series A: proven model. Time to scale. £2M to £10M+.

Series B, C, D: bigger rounds, bigger funds, bigger expectations.

Bridge round: a top-up between proper rounds. Often a warning sign.

Down round: a new round at a lower valuation than the last. Painful.

Exit: acquisition or IPO. The moment your investors get their return.

Paperwork & process

Term sheet: non-binding offer. Sets the headline terms of the deal.

SAFE / Convertible loan note (CLN): money in now, equity issued later. Defers the valuation conversation.

Vesting: you earn your shares over time, usually four years. Stops one founder walking off with everything.

Cliff: no shares vest until a set date. Standard is 12 months. Quit before then, you get nothing.

Share options (EMI scheme): the right to buy shares later at today's price. Used to compensate staff. EMI is the UK-specific, tax-friendly version.

Liquidation preference: investors get their money back first if you exit. Watch the multiplier here.

Pro-rata rights: an investor's right to keep their % in your next round.

Due diligence (DD): the forensic check before they wire the money.

One quick clarification: "share options" and "options" mean the same thing in this context. The right to buy shares later at a fixed price. They are different from the shares themselves. Founders get shares. Early employees usually get options.

If any of those terms still feel fuzzy, fix that this week. Bookmark this section. Reread it before every meeting.

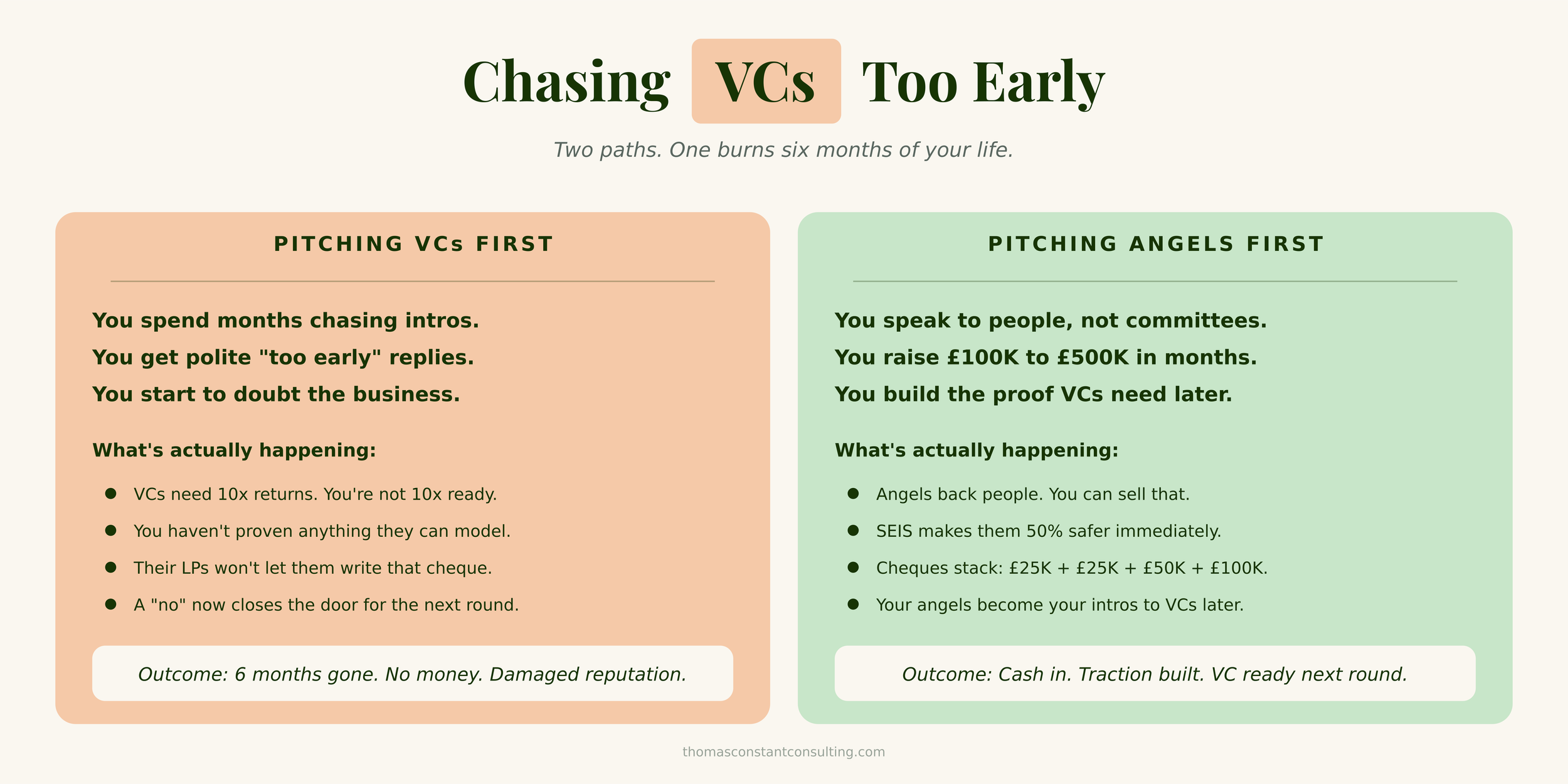

3. Stop Chasing VCs. They're Not Reading Your Email Anyway.

This is the single most expensive mistake I see early-stage founders make.

You finish the deck. You feel ready. You start LinkedIn-stalking partners at Atomico, Balderton, Octopus, Index. You spend three weeks crafting the perfect cold email. You send it. You get nothing back. You convince yourself it's the email. You send another. And another.

It's not the email. They're not the right audience. Not yet.

VCs run funds. Funds have Limited Partners. Those LPs expect a 10x return on the whole fund. To make their model work, every cheque a VC writes needs to have a credible path to a £100M+ outcome. That's the maths.

If you have an MVP and a hundred users, that maths doesn't work yet. It's not personal. They literally cannot write you a cheque without breaking their own model. The "too early" reply is genuine, not a fob-off.

Here's the thing nobody tells you. Their "no" now isn't neutral. It closes the door. When you come back in 18 months with real traction, they remember. You've burned the relationship before it started.

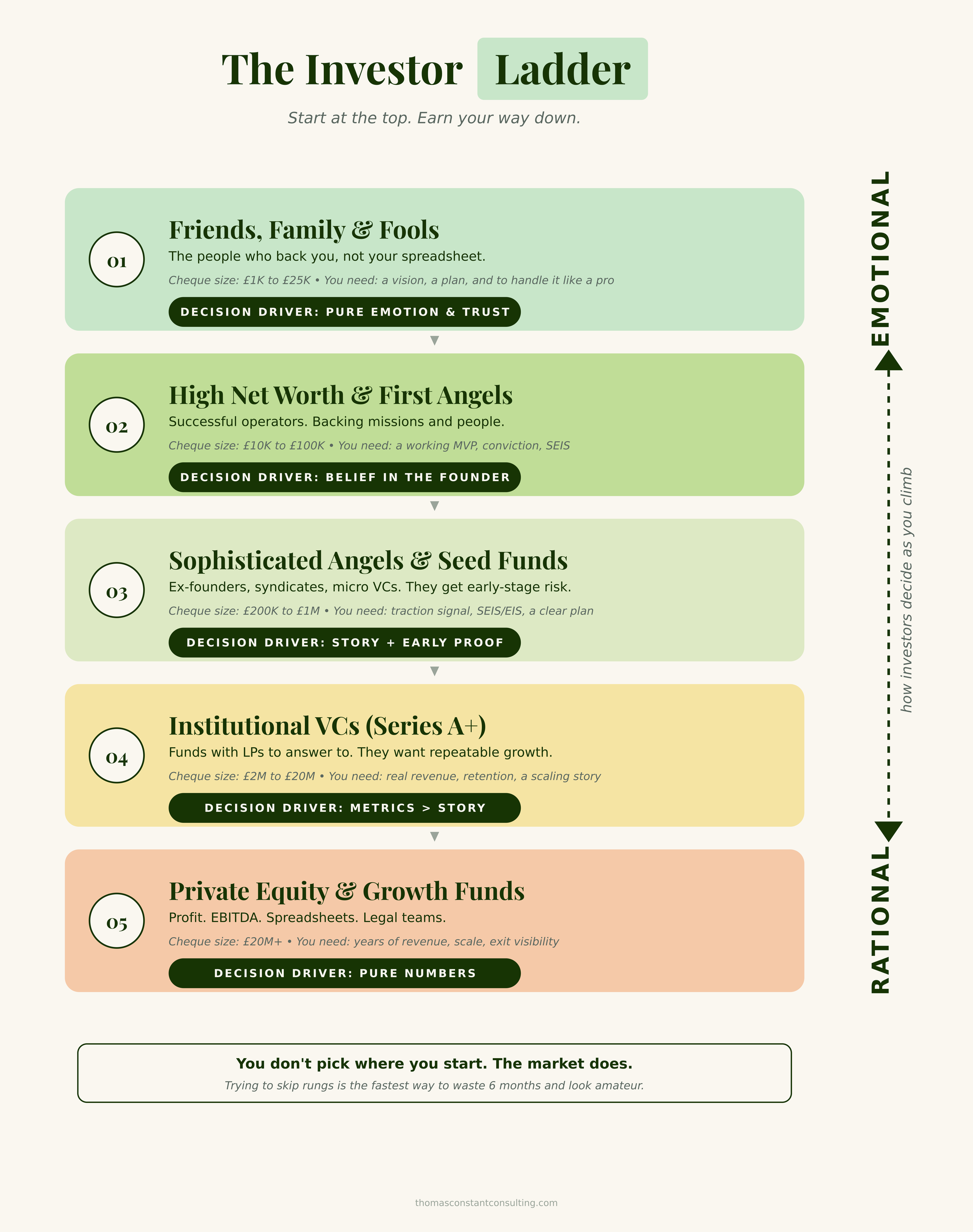

So what do you actually do? You climb the ladder.

The bottom of the ladder is emotional. The top is rational. As you climb, the maths gets harder and the love gets thinner.

Rung 1: Friends, Family & Fools. The first £1K to £25K usually comes from people who back you, not your spreadsheet. Treat them like proper investors anyway. Send a one-pager. Sign proper paperwork. Set expectations honestly. SEIS applies here too.

Rung 2: High Net Worth & First Angels. Successful operators, self-certified HNW individuals, people who've made money and want to put some of it into early-stage companies. Cheques £10K to £100K. They back missions and people. SEIS makes them 50% safer immediately.

Rung 3: Sophisticated Angels & Seed Funds. Ex-founders, syndicates, micro VCs, early-stage seed funds. They get early-stage risk because they've lived it. Cheques £100K to £1m. They want story plus early proof.

Rung 4: Institutional VCs (Series A+). Funds with LPs to answer to. They want repeatable, modelable growth. Cheques £2M to £20M. Decisions are driven by metrics, not by how charming you are over a flat white.

Rung 5: Private Equity & Growth Funds. Profit, EBITDA, spreadsheets, legal teams. Cheques £20M+. You need years of revenue and a clear path to exit. This isn't your world for a long time.

Here's the rule:

You don't pick where you start. The market does.

If you're pre-revenue with an MVP, you're starting at rung 1 or 2. Trying to skip rungs is the fastest way to waste six months and look amateur.

The right move is to stack small cheques from people on the rungs you actually belong on. Use that capital to build proof. Then climb.

Your angels become your warmest intros to seed funds. Your seed funds become your warmest intros to VCs. The ladder builds itself if you don't try to jump it.

4. Build a Strong Data Room (It's Just a Folder, But It Matters)

Forget pitch decks for a minute. This is the section that decides whether you actually get funded.

Getting investment ready IS getting you AND your data room ready. It is everything an investor expects to see when they start asking serious questions. Pitch deck, investment memo, cap table, financials, IP, contracts, traction proof. All of it. In one organised place. Categorised so they can find what they need without asking.

Here is the truth about most early-stage founders: you already have most of this information. It is just scattered. Some of it lives in your inbox. Some on your laptop. Some in your head. Some is half-finished and looks unprofessional. Some you have not created yet because nobody has ever asked for it.

Investment ready means doing the work to centralise, collate, and create everything an investor needs, in one organised, professional folder. It is a forcing function. The act of building the data room is the act of becoming investable.

If you cannot fill it in, you are not ready to raise. If you can fill it in but it looks rushed, you are not ready either. Investors are not just buying your idea, they are buying how you operate. The data room is the clearest proof of that.

Practically, a data room is just a well-organised, shareable folder. Google Drive, Dropbox, Notion, OneDrive. The platform does not matter. What matters is structure, clarity, and ease of use. It needs to be:

Clean: easy to navigate.

Credible: accurate and up to date.

Complete: includes the right documents.

Your data room is not static. As your company grows, so does your data room. By Series A, you will need deeper financials, compliance documents, employment contracts, and more. The structure and discipline you build now makes future rounds faster, smoother, and more professional.

Core sections of a strong data room:

1. Company overview

One-pager

Pitch deck

Investment Memorandum

2. Company structure & legal docs

Company incorporation certificate

Articles of Association

Shareholder agreements

Cap table (who owns what, and how that changes post-raise)

IP documentation (patents, trademarks, copyright registration)

SEIS/EIS Advance Assurance letter

3. Financials

Profit and loss statement (if applicable)

5-year financial projections

Any existing investor commitments

Details of loans or debt facilities

4. Product & traction

Product or demo links

Tech architecture (for SaaS or tech businesses)

Pilot results or case studies

Customer testimonials or reviews

Sales pipeline reports or revenue figures (if applicable)

Market research, original or third-party

5. Team & advisors

Founder bios and LinkedIn profiles

Team structure or org chart

Advisory board or mentors

Any key hires planned with the raise

6. Commercial & contracts

Signed contracts, LOIs, MoUs

Strategic partnerships

Terms of service and privacy policy (for online platforms)

Grant award letters or funding confirmations

Why this all matters

Many early-stage startups don't have much traction yet. That's okay. You're not expected to be perfect, but you are expected to be transparent, thoughtful, and prepared.

If you're missing a document, say so. Your projections are educated guesses. That's fine. Just show your logic. If something's still in progress, give a timeline.

You are showing investors how you think, how you work, and how you lead. The more organised, open, and detail-aware you are, the more confident they'll be.

Investors aren't just investing in your idea. They're investing in you. The data room is one of the clearest reflections of that.

One last thing: how to actually build the Company Overview pieces.

This is the part of the data room investors hit first. The one-pager, the pitch deck, and the Investment Memorandum. Get this right and the rest of the data room gets a fair hearing. Get it wrong and they never open the other folders.

Here is the order to build them in: backwards.

Start with the Investment Memorandum. This is the master document. Everything an investor could reasonably want to know about your business, written out in full. Vision, problem, solution, market, model, team, financials, the raise, the risks etc etc. It is long and that is the point. Writing it forces you to actually understand your own business from every angle

Then condense it into a pitch deck. 10 to 12 slides max. The high-level overview. Story-led. Designed to support you when you are talking, not replace you. Strip out everything that is not essential.

Then boil that down into a one-pager. A single page that gets the door open. Just enough for an investor to want a meeting. Nothing more.

If you build them the other way round, starting with the one-pager, you end up with a deck full of slogans and an IM with no depth. Always start at the bottom and compress upward.

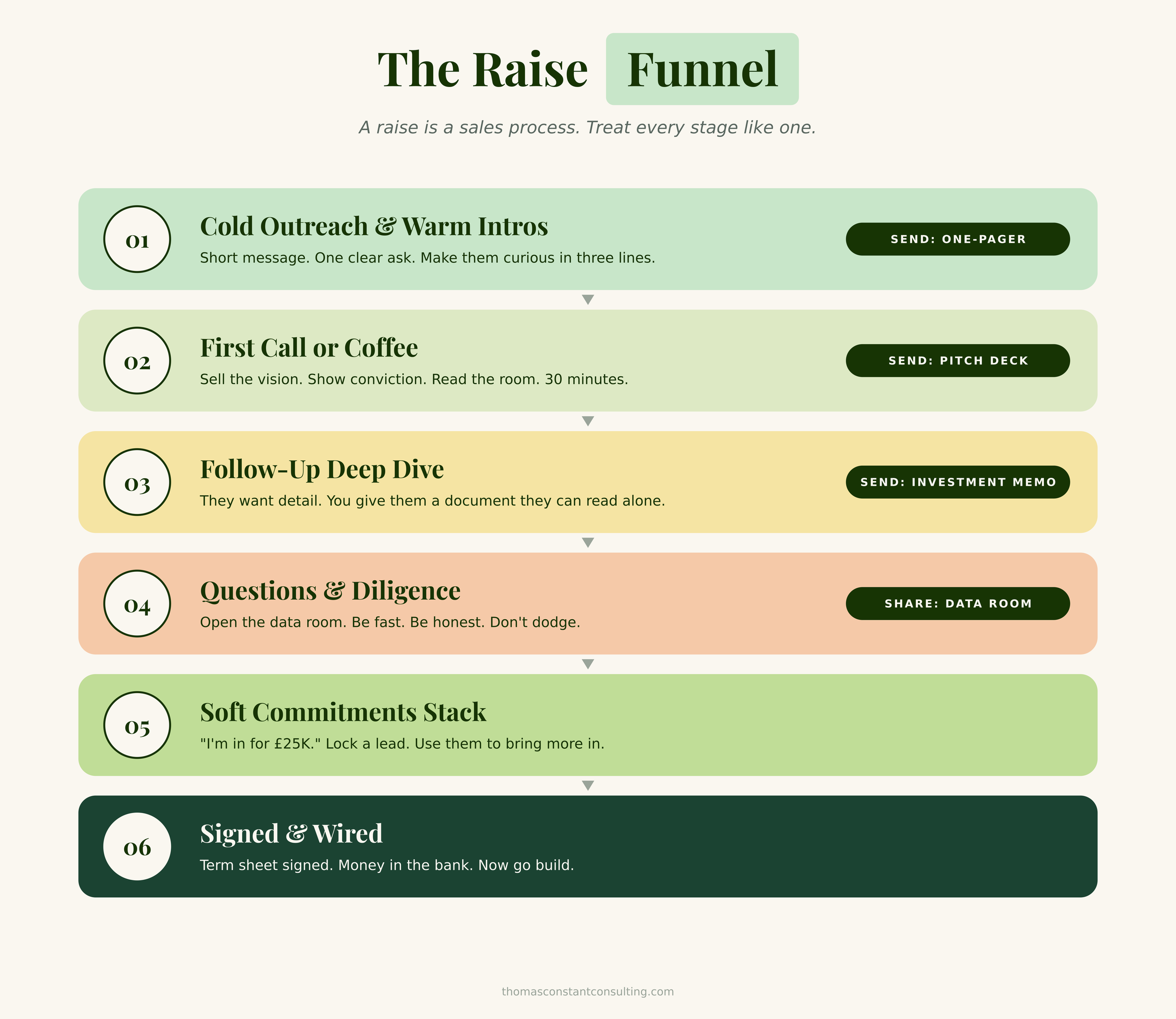

5. Selling the Vision: It's a Sales Process, Not a Pitch

Let's get one thing straight. This isn't about decks. It's about selling a compelling vision of the future and getting investors to believe you're the one to build it.

You're not just pitching information. You're selling a story. (For the actual storytelling craft, the structure of your "why", and how to land emotional hooks.. This section is about the process around the story.) Your job is to guide investors through a journey of trust. Start broad. Get deeper as they lean in. Treat it like a sales funnel.

Stage 1: Cold outreach & warm intros. Short message. One clear ask. Make them curious in a few lines and attached the one-pager. The aim here is to get a call.

Stage 2: First call or coffee. Sell the vision. Show conviction. Read the room. 30 minutes max. The deck supports you, it doesn't replace you. Keep slides visual and minimal. Frame the problem with urgency, reveal the solution in one clean sentence, show real traction (not vanity metrics), outline the market clearly, prove your team's credibility, tease the model, state the ask. The aim here is to get a 2nd meeting.

Stage 3: Follow-up deep dive. They want detail. You give them your Investment Memorandum, a long-form document they can read alone. Vision, problem, solution, market, business model, competition, go-to-market, traction, team, financials, the raise etc etc. Paragraphs and charts, not bullet soup.

Stage 4: Questions & diligence. Share the full data room.

Stage 5: Soft commitments stack. "I'm in for £25K." Not legally binding, but it builds momentum. Use a soft lead to bring more in. £10K here, £50K there, £250K from a syndicate. Bit by bit until the round fills.

Stage 6: Signed & wired. Term sheet signed. Money in the bank. Now go and build the thing you said you'd build.

Most no's happen at stages 1 to 3. Make those tight before you scale outreach.

6. Inside the Angel Investor's Head

Angel investors are real people. Not dragons. Not sharks. People. Usually successful operators, exited founders, or business veterans who want to give back and grow their wealth.

They're not just investing for financial return. They're backing missions, people, and energy. They want to feel something. That's why storytelling matters. That's why your conviction matters.

At the early stage, angels know there's massive risk. Most of their investments won't return. So when they back someone, it's rarely about a flashy deck. It's about what they feel about the founder and the vision.

They're looking for:

Founders who are credible, coachable, and committed.

Problems that are big, painful, and worth solving.

Opportunities that can scale, not just scrape by.

Markets they understand, care about, or are curious about.

Chemistry. They need to like you and believe in you.

They want to see you've done your homework. That you know your numbers. That you're not bullshitting. Show up with structure, with passion, and as yourself.

7. SEIS & EIS: Your UK Superpower

This is the single biggest unfair advantage UK founders have, and so many of you don't use it properly.

SEIS (Seed Enterprise Investment Scheme) and EIS (Enterprise Investment Scheme) let your investors claim back up to 50% of their investment in income tax relief. They also avoid Capital Gains Tax on profits, and can offset losses against income tax if it all goes wrong. The maths is wild.

This de-risks their decision massively. Which makes them far more likely to invest. Which makes you far more fundable.

You apply via HMRC. It's free. You'll need a business plan, cap table, and pitch deck. Submit it, wait a few weeks, and you get back an Advance Assurance letter. That's your golden ticket.

Investors will ask: "Do you have Advance Assurance?"

You want to be able to say: "Yes. Here's the letter."

If you don't have it, get it before your first investor call. Not after. Before.

Apply here > HMRC SEIS Application

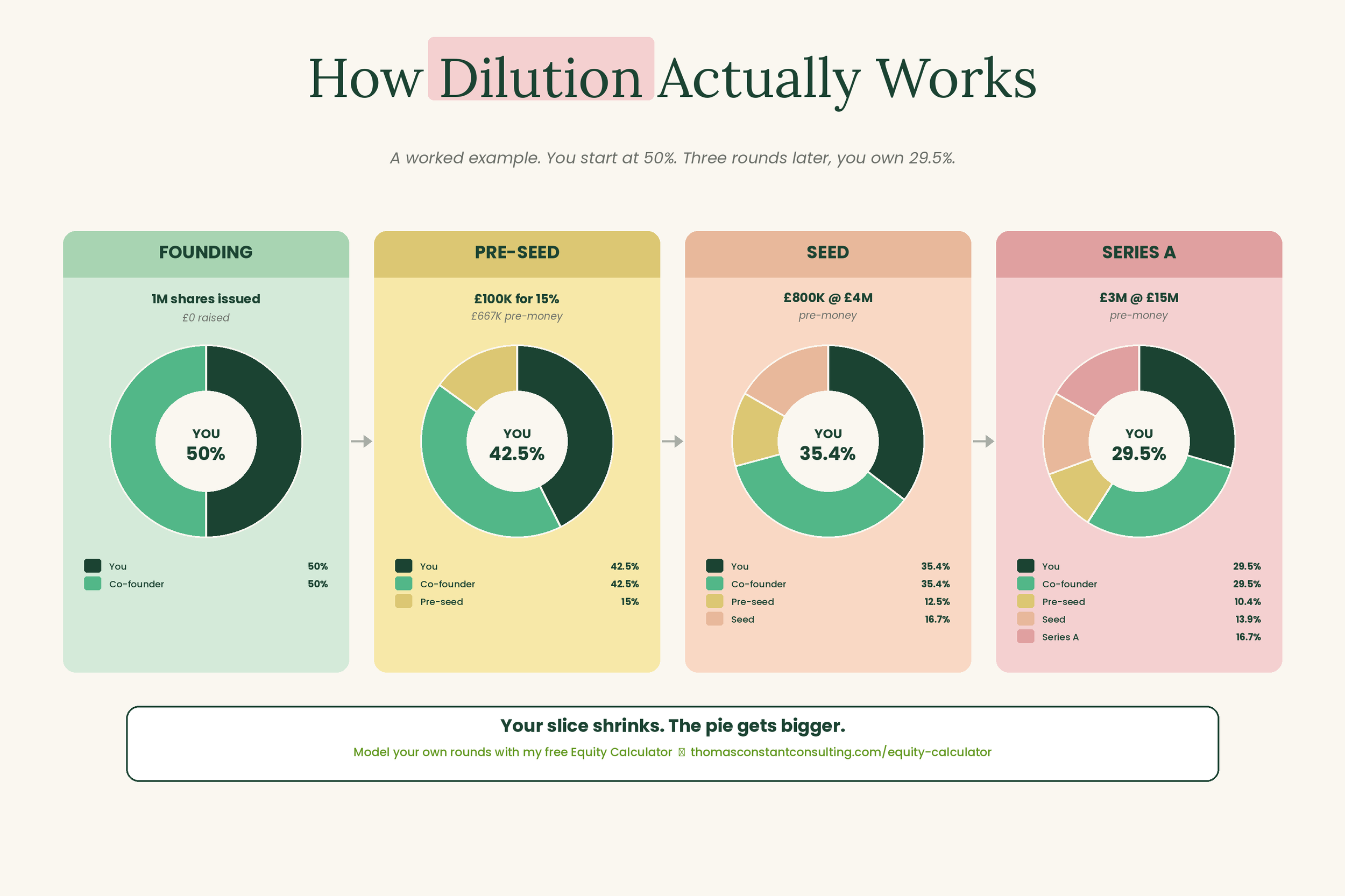

8. Valuation: Educated Guesswork With Real Stakes

One of the most confusing and most important parts of raising money: valuation. For the first time.

A valuation is the price tag you (or your investors) put on your company. It determines how much of your business you give away in exchange for investment.

If you raise £250K at a £1M pre-money valuation, you're giving away 20% of the business (because £250K is 20% of £1.25M post-money).

Higher valuation = less dilution. Lower valuation = more equity given away.

So yes, it's in your interest, and your duty to your co-founders and team, to aim for the highest reasonable valuation you can defend.

But how do you value an early-stage startup? You don't have profit. Often you don't even have revenue. So it's not traditional financial modelling. It's a mix of:

Traction: the more proof (users, revenue, waitlist, retention), the more credible the number.

Team: experienced or repeat founders justify higher numbers.

Market size: bigger market, bigger upside.

Vision: can investors see this becoming a £10M, £100M, £1B+ outcome?

Comparables: what are other startups in your space raising at?

Defensibility: IP, first-mover advantage, real moat.

Valuation isn't a science. It's a negotiation. You're selling belief in your future. They're buying into risk. There's always give and take.

Tips for setting one:

Look at recent UK raises on Beauhurst, Crunchbase, or Dealroom to see what's typical for your stage.

Ask friendly angels or founders what they raised at.

Don't go too high too early. You'll set expectations that hurt you next round.

Don't sell yourself short either. Undervaluing now means unnecessary dilution and can make you look naive.

Use SEIS and EIS to your advantage. They reduce investor risk, which can justify higher valuations.

If you can't confidently set a valuation, raise via a SAFE or convertible loan note. These defer the valuation to a future round, usually with a cap (maximum valuation) and a discount (incentive for early investors).

Want to model what your dilution looks like across rounds? I built a free Equity Calculator for exactly this. Plug in your numbers and see what you actually own at the end. thomasconstantconsulting.com/equity-calculator

And remember: every % you keep now is worth 10x more if you make it. So fight for it. Wisely.

Hope this helps. Tom

——————————————————

🧠 The TL;DR

Raise for the right reason. Not ego. Raise to hit a milestone.

Learn the language. If you can't define a term, don't book the meeting.

Don't chase VCs from day one. They can't write your cheque even if they wanted to. Start at the bottom of the ladder.

Plan for 18 to 24 months of runway. Anything less and you're back fundraising before you've shown traction.

Build a clean data room. Pitch deck, IM, legals, financials, traction. Investors are buying your organisation as much as your idea.

Treat the raise as a sales process. One-pager → deck → IM → data room → soft commit → close.

Get SEIS/EIS Advance Assurance before your first call. Not after.

Defend your valuation with logic. Don't pluck a number, don't undersell yourself.

———————————

———————————

🧠 Core Reads

Angels by Jason Calacanis — a sharp, no-fluff guide to how angel investors think, what they look for, and how to actually get a yes.

Venture Deals by Brad Feld & Jason Mendelson — the standard reference on term sheets, valuation, and investor dynamics. If you're raising equity, read this

The Lean Startup by Eric Ries — the OG framework on MVPs and validated learning. Still relevant.

The SEIS/EIS Guide b — everything you need to know about the UK's biggest early-stage investment advantages. HMRC

Y Combinator Library — Free. Modern. The best collection of founder essays on the internet.

Want Help Applying This to Your Startup?

♻️ Book a free 30-minute Investment Readiness Clarity Call. No pitch required. Just an honest conversation about where you are and what to focus on next.

🔔 Book your free call at thomasconstantconsulting.com