The Art of the Pitch

Overview of this article:

Pitching isn't presenting: why most founders are doing the wrong thing entirely, and what a real pitch actually is.

Your words matter less than you think: the science behind why energy, presence, and belief carry more weight than your slides ever will.

Know your room: the five audiences UK founders typically pitch to, and what each one actually wants to hear.

The Framework: Y Combinator's 6-part investor pitch structure, and how to use it.

The 7 questions every investor is silently asking: understand these and you'll never fumble a pitch meeting again.

Momentum beats revenue: why a fast-moving startup with £0 revenue could be more fundable than a slow one with £1m.

Common mistakes: the things founders get wrong every single time, and how to avoid them.

Read time: 15 minutes

Best for: UK founders preparing to pitch investors, accelerators, or grant bodies for the first time. Pre-seed to early seed.

——————————————————

Most founders prepare the wrong thing.

They spend weeks perfecting the deck. Tweaking the font. Agonising over the market size slide. And then they walk into the room, open the laptop, and start presenting.

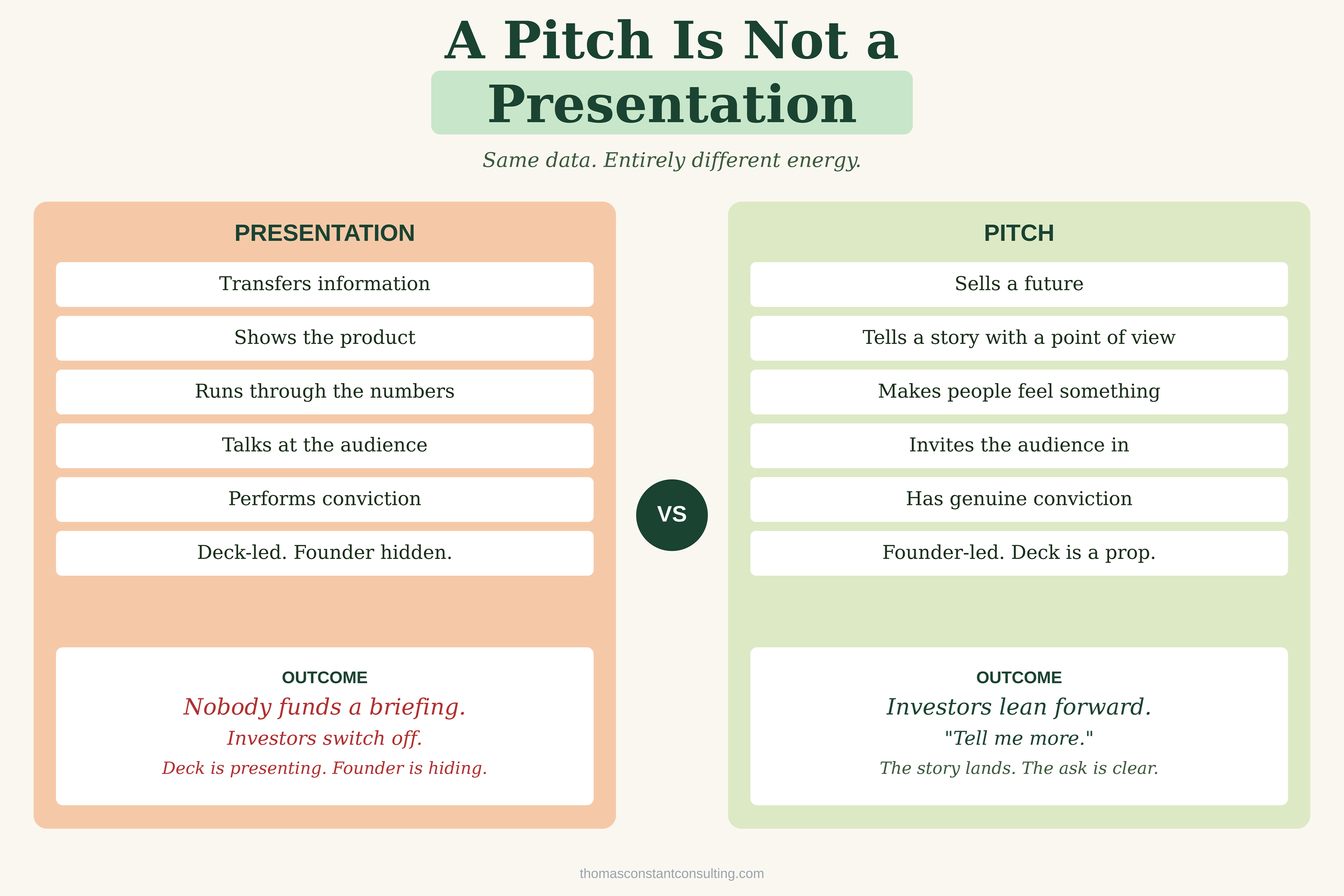

That's not a pitch. That's a briefing. And nobody funds a briefing.

A pitch is something completely different. It's a story. It has a point of view, an emotional arc, and a clear ask. It makes people feel something. And feeling something is what gets people to act.

I've pitched to angel investors, grant panels, accelerator programmes, and enterprise partners. I've made every mistake in the book. And I've also seen the moment when it clicks, when someone leans forward in their chair and says "tell me more." That moment doesn't come from a brilliant slide. It comes from a brilliant story, told by someone who believes it.

This article is Part 4 of the UK Startup Playbook. It's everything I wish someone had told me before my first pitch. Let's get into it.

This is Part 4 of the UK Startup Playbook. If you haven't read the earlier parts yet, start with Part 1:How to Tell If Your Idea Is Worth Anything, then work through Part 2: How to Get Funded, Part 3: Investment Readiness. They all feed into this one.

——————————————————

1. Pitching Isn't Presenting

Before you book a single pitch meeting, get clear on one thing: there is a fundamental difference between a presentation and a pitch. Most founders treat them like the same thing. They are not.

A presentation transfers information. It says: here is the market, here is the product, here are the numbers. That's fine for a board update. It's death in a fundraising room.

A pitch sells a future. It says: here is the world as it is, here is the problem that nobody has solved properly, here is why we're the ones to fix it, and here is what that looks like if you back us. Same data, entirely different energy.The best pitches don't feel like pitches at all. They feel like someone sharing a bold, clear, personal vision and inviting you to be part of it. That's the target.

Before you write a single slide or rehearse a single line, ask yourself two questions:

What do I want the audience to feel?

Do I actually feel that?

If you don't feel it, they won't either. Investors have been in too many rooms, heard too many pitches, and seen too many founders who believe their own hype. They can smell the difference between someone who is performing conviction and someone who actually has it.

So start there. Not with the deck. Not with the market size. With your genuine belief in what you're building.

2. Your Words Matter Less Than You Think

Here is something that should make nervous founders feel better, and overconfident ones feel uncomfortable: the words in your pitch carry less weight than almost everything else.

Dr Alex Pentland at MIT spent years studying what he calls "honest signals", the nonverbal cues that humans unconsciously send and receive in communication. His research found that good communication has very little to do with your actual words. The things that really move people are energy, pace, presence, conviction, and the subtle signals you send about how much you believe in what you're saying. That MIT research lands very close to something Michael Seibel, Managing Partner at Y Combinator, has been saying to founders for years from the other side of the table: you don't need pizazz. You don't need shark tank energy. You stand out by being concise and easy to understand.

Those two things sound like they're in tension, but they're not. Calm clarity is the energy. A founder who can explain what they do in two sentences, without jargon, without hedging, without over-explaining, signals something very powerful: they understand their business.

Michael has done over 2,000 YC interviews. The single most common reason founders don't get funded? Investors don't understand what the company does. Not because investors are slow. Because the founders haven't got clear yet.

"The number one barrier to investors not knowing what your company does is you." — Michael Seibel, Y Combinator

The lesson: before you practise the pitch, practise the clarity. Can you explain what you do to a stranger in one sentence? Can you say it to your grandmother and have her understand it? If not, you're not ready to pitch yet.

3. Know Your Room

One of the biggest mistakes early-stage founders make is walking into every pitch with the same script. It doesn't matter how good that script is. If it's not calibrated to the audience, it won't land.

Here are the five audiences UK founders most commonly pitch to, and what each one actually wants to hear.

Angel Investors: Angels are individuals writing personal cheques, usually £10K to £100K. They back people as much as products. At this stage, they want to believe in you, believe in the problem, and feel like the market is real. SEIS and EIS matters here too: the UK's tax relief schemes mean a well-structured deal immediately cuts their downside by up to 50%. Lead with mission, back it with traction, make the numbers digestible.

Accelerator Panels: Accelerators are backing potential, not proof. They want to see a coachable founder with a clear problem and early signs of momentum. What they're often scoring you on: how clearly you understand your customer, whether your team has the right combination of skills, and whether you're the kind of person who will actually take feedback and run with it. Humility matters here as much as ambition.

Grant Assessors: Grant bodies, whether Innovate UK, local growth hubs, or EU funds, might not be looking for a financial return. They're looking for impact, evidence, and deliverables. They want to know exactly what you're going to do with the money, what you'll prove, and how it connects to a broader innovation or social mission. The pitch here is less emotional and more evidential. Numbers, milestones, outcomes. If your startup has an impact or SDG angle, lean into it hard.

Enterprise Partners and Customers: When you're pitching a potential customer or commercial partner, the job is de-risking. They're not investing money; they're investing time and credibility. They want to know: does this actually work? Who else has trusted you? What does implementation look like? Lead with results and remove as much friction as possible.

Competition Judges: Competition judges have usually heard twelve pitches before yours. What they remember are the ones that gave them a moment, a line, a stat, an image, something that stuck. You're not trying to win on completeness. You're trying to win on memorability. Be sharp. Be bold. Leave one thing in their heads.

4. The Three Pitch Formats

Before you start building any pitch, get clear on which format you're actually preparing. There are three. Each one has a completely different job, and confusing them is one of the most common and costly mistakes founders make.

The 30-Second Elevator Pitch: This is the version you need everywhere: networking events, chance encounters, introductions at demo days. Three things and nothing more: what the problem is, what you do about it, and who you are. The goal isn't to close anyone. The goal is to earn a longer conversation. If someone says "that's interesting, tell me more", you've won.

The 5 Minute Pitch: Add traction, credibility, and a clear ask. This is the pitch you give at accelerator open days, early investor intros, and warm networking follow-ups. You now have space to bring in a story, set up the problem with some texture, and land the ask cleanly. Still no deck required. This one lives or dies on how well you've rehearsed it out loud.

The 10+ Minute Full Pitch: The full narrative arc with a deck. This is your Series A prep, your pitch competition slot, your proper investor meeting. You now have room to walk through the business, your insight, your traction, your team, and your ask in a structured way. Even here, the rule holds: the deck is a prop, not the pitch. You are the pitch.

5. The Seibel Framework: How to Structure an Investor Pitch

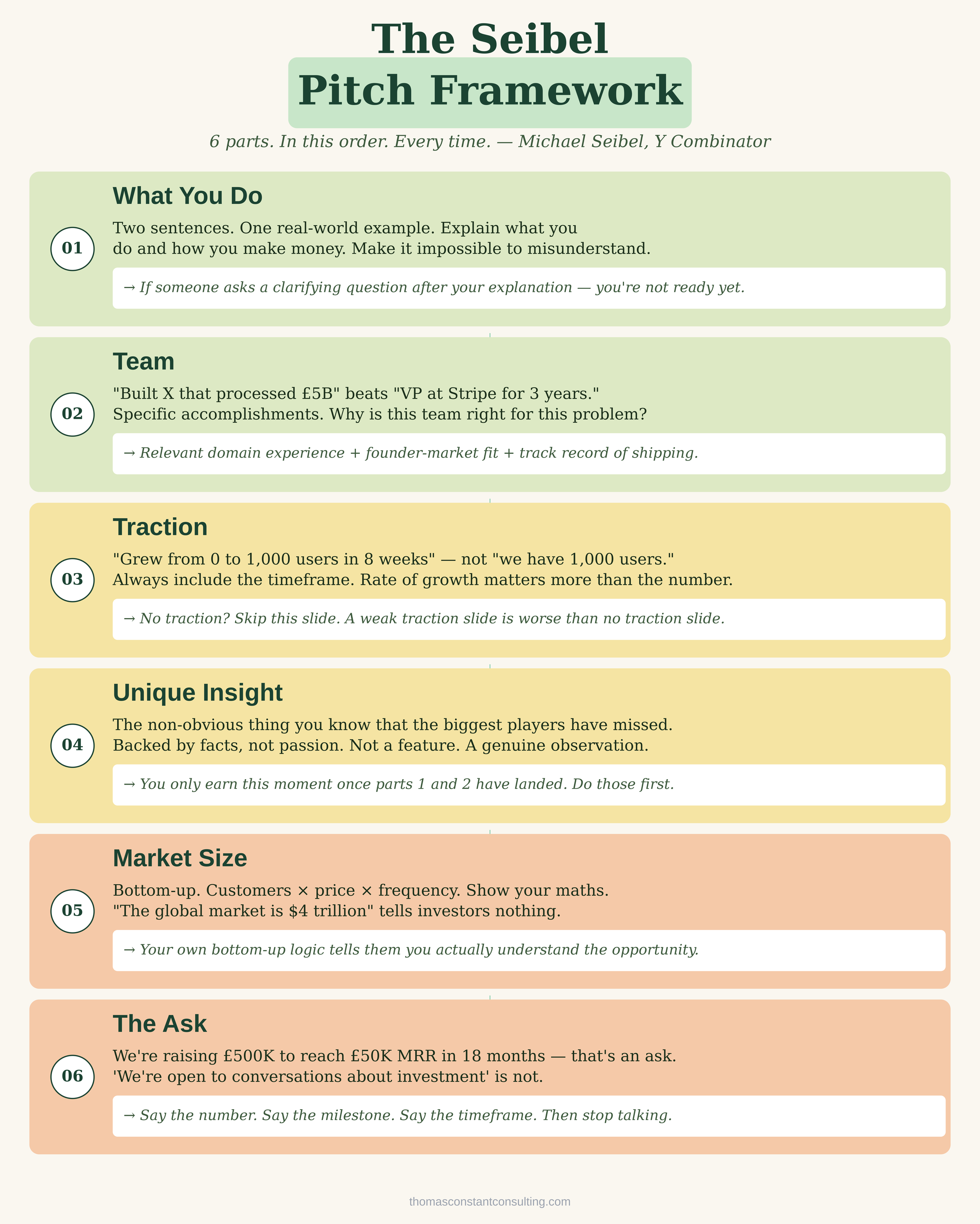

Michael Seibel, Managing Partner at Y Combinator, has reviewed more investor pitches than almost anyone alive. After 2,000+ YC interviews and years of watching founders raise and fail to raise, his framework for a seed-stage investor pitch has six parts. In that order. Every time.

There is no single perfect pitch deck structure. But this is as close to a universal framework as exists. And it works because it's built around what investors actually need to hear, not what founders want to say.

Part 1: What You Do

Two sentences. One specific, real-world example. That's it.

The two sentences explain the mechanism: what your company does and how it makes money. The example makes it concrete and human. Without the example, even a clean description can still feel abstract. Seibel uses Airbnb as the benchmark. Their two-sentence description: they let any homeowner rent out their place online. They handle the payment and take 15% per booking. Clear. Specific. No jargon. Anyone can picture it immediately.

Your test: explain what you do to someone who has never heard of your sector. If they get it immediately, you're there. If they ask a clarifying question, you're not ready yet.

Part 2: Team

This is where most founders go wrong. They list titles. They describe years at companies. They mention that they went to a good university.

None of that matters as much as specific accomplishments. There is a big difference between "Jane was VP Engineering at Stripe for three years" and "Jane built the payment infrastructure at Stripe that processed £5 billion annually." Same person. The second version tells you something real about what she can do.

Your team slide should answer one question: why is this the right team to solve this specific problem? Relevant domain experience, founder market fit (have you lived this problem?), and any track record of building and shipping things. If your team has done something that has made investors money before, say it.

Part 3: Traction

Traction is not just revenue. It's proof of momentum. The key word in every traction statement is the timeframe.

"We have 1,000 users" tells an investor almost nothing. "We grew from zero to 1,000 users in eight weeks" tells them you can move fast. Investors fund momentum, not absolute numbers. The rate of growth matters more than where you are right now.

Traction at early stage can be: users, revenue, pilot customers, letters of intent, completed interviews that converted to paying customers, or a product shipped from nothing in a short window. All of it counts. Include the timeframe every single time. One critical rule from Seibel: if you have no traction, do not include a traction slide. A weak traction slide is worse than no traction slide. It signals that you don't understand what investors are looking for. Skip it and talk about the team instead.

Part 4: Unique Insight

This is the most intellectually interesting part of a pitch. It's also the part most founders rush, skip, or get wrong.

Your unique insight is the non-obvious thing you know about this problem, this customer, or this market that the biggest players have missed. It's not a feature. It's not a USP statement. It's a genuine observation that, once heard, makes the investor think: "Oh. They actually understand something real here."

Seibel's Airbnb example: every home-sharing product that came before Airbnb failed to process payments in the booking flow. Hosts and guests both wanted to transact, but doing it in a low-trust environment felt too risky. Airbnb solved that. The insight wasn't just "people will rent out their homes." It was "the payment problem is the entire problem."

Your insight needs to be backed by facts or first-hand evidence, not just a hunch. And you only earn the right to land this point if the investor already understands what you do and respects your team. Get parts one and two right first.

Part 5: Market Size

Here is where most pitch decks die a slow, painful death. A giant TAM number with no logic behind it. "The global market is $4 trillion." Fine. What does that have to do with you?

Seibel's approach: show your work. Build the market size from the bottom up. How many potential customers are there? What would they pay? What's your realistic share over what timeframe? Walk through the maths out loud.

Bottom-up market sizing signals that you actually understand your customer. It's more credible, more interesting, and harder to dismiss than a top-down TAM slide copied from a McKinsey report. The goal isn't to impress investors with the size of the number. It's to demonstrate that you understand the opportunity clearly enough to model it.

Part 6: The Ask

Say the number. Explicitly. Directly. Then stop talking.

Most founders dance around the ask. They say things like "we're looking to raise a round" or "we're open to conversations about investment." That is not an ask. That is a conversation starter. It leaves money on the table from investors who would have said yes.

Your ask should include: the amount you're raising, what milestone it gets you to, and the timeframe. "We're raising £500K to get to £50K MRR over the next 18 months" is an ask. It's specific, it's tied to a goal, and it makes it easy for an investor to evaluate whether it's credible.

Also say who else has invested if anyone has. Social proof in early rounds is powerful. If a credible angel is already in, other investors are much more likely to follow.

6. The 7 Questions Every Investor Is Silently Asking

While you're talking, investors are running a parallel track in their heads. They may not interrupt. They may not show it on their face. But these are the seven questions that are playing out in real time throughout every pitch.

Know them. Answer them, even the ones nobody asks out loud…

These questions map almost directly onto the Seibel framework above. That's not a coincidence. The framework exists precisely because it answers what investors are actually trying to figure out.

7. The Pitch Deck Structure That Works

There is no single perfect pitch deck. Anyone who tells you otherwise is selling a template. But there is a structure that most investors are familiar with, expect to see, and can navigate quickly. Start here and adapt from it.

The ten sections of a solid investor deck:

Overview: One slide. What you do in two sentences. Make it impossible to misunderstand.

The Problem: Define the enemy. What is the specific, painful, expensive problem that exists right now? Make the investor feel it. Quantify it where you can.

The Solution: What you've built. Not a feature list. A clear, specific answer to the problem you just made the investor feel.

Market Opportunity: Bottom-up market sizing. Number of potential customers, times price, times realistic frequency. Show your work.

Business Model: How you make money. Simple. One slide.

Competition: Who else is in this space and why you win. Don't pretend there are no competitors. Show the comparison and explain your edge.

Traction: Don't say it, show it. Real numbers. Real timeframes. If the traction isn't impressive yet, skip this slide entirely.

Team: Specific accomplishments, not titles. Why this team. Why now.

Financial Projections: Five years is standard. Be honest about your assumptions.

The Ask and Next Steps: Amount, milestone, timeline. Clear and direct.

One design rule across all of it: boring slides are better than beautiful ones. A deck that makes the investor look at you instead of the screen is doing its job. Whitespace, clear typography, real numbers. That's it.

8. Momentum Beats Revenue

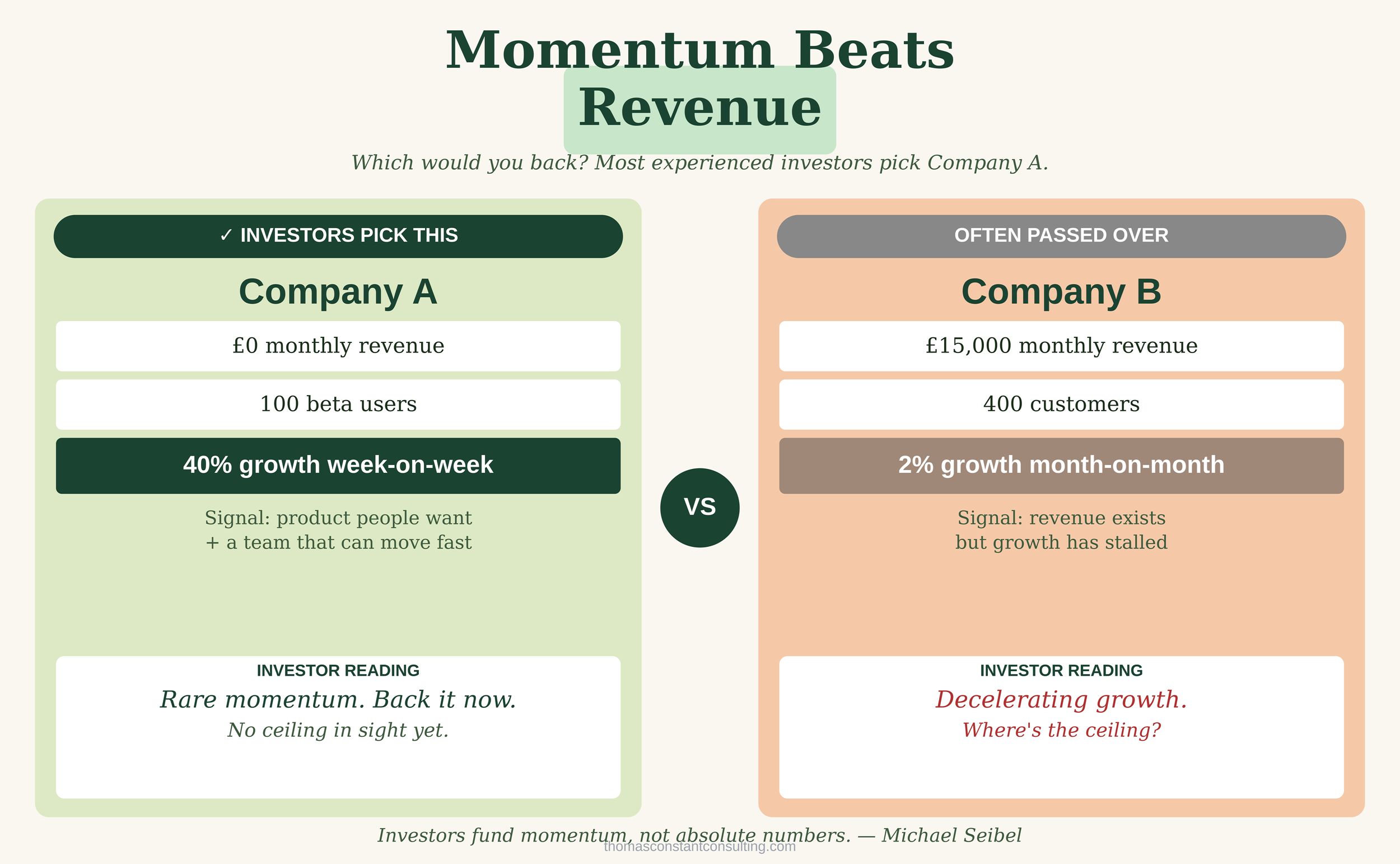

Here's one that trips up a lot of early-stage founders. They look at their numbers, decide they're not impressive enough to pitch, and wait. That is usually a mistake.

Consider two companies. Company A has £0 monthly revenue, 100 beta users, and is growing 40% week on week. Company B has £15,000 monthly revenue, 400 customers, and is growing 2% month on month.

Which would you back?

Most experienced early-stage investors pick Company A without hesitation. The rate of growth is the signal. A startup doubling every few weeks with no revenue is showing something rare: a product that people want and a team that can move. A startup with revenue but decelerating growth is showing something investors don't like: a ceiling.

Investors fund momentum, not absolute numbers.

Present your traction with the timeframe front and centre. "We grew from zero to 500 users in six weeks" is a better line than "we have 500 users." Same fact. Different story.

9. Common Mistakes

These are the things I see founders get wrong every single time. Some of them I've made myself.

Spending too long on the solution: You have a limited window. Most founders use half of it setting up the problem in exhaustive detail and run out of time before the ask. The problem needs to land fast. One or two slides maximum. Then move.

Scripting instead of rehearsing: There is a difference between practising a script and rehearsing a pitch. Scripts break the moment someone asks a question you weren't expecting. Rehearsal builds fluency. Know your material so well you can have a conversation about it, not recite it.

Faking traction: Advisor surveys. Social media followers. Press mentions. None of these are traction. If you don't have real traction yet, don't include a traction slide. Talk about the team instead.

Not making a direct ask: If you don't ask, you won't get.

Not controlling the Q&A: Anticipate the hard questions. Prepare sharp, honest answers. Don't bluff. If you don't know the answer, say so and tell them how you'll find out.

Cluttered messaging: Every slide should have one job. Cut your deck by a third and your pitch by half. What's left will be sharper.

——————————————————

——————————————————

The TL;DR

1. A pitch is not a presentation. One transfers information. The other sells a future.

2. Clarity is the whole game. The number one barrier is you.

3. Different audiences, different pitches. Adapt the angle, not the story.

4. Use the Seibel Framework. What you do, team, traction, unique insight, market size, ask. In that order. Every time.

5. Know the 7 questions investors are silently running. Answer them before they ask.

6. Momentum beats revenue at early stage. Lead with your growth rate and always include the timeframe.

7. Don't fake traction. Don't hide from the ask. Don't script what should be a conversation.

Want Help Applying This to Your Startup?

♻️ Book a free Investment Readiness Clarity Call. No pitch required. Just an honest conversation about where you are and what to focus on next.

🔔 Book your free call at thomasconstantconsulting.com